-

Address: 10430 FM 1097 W WILLIS, TX 77318

-

Phone: (936) 465-9981

-

Email: service@tghinsurance.com

Most contractor insurance problems don’t show up when you buy the policy.

They show up when a GC requests a certificate… when you hire your first employee… when a truck gets into a fender-bender… or when a jobsite loss happens and the claim comes back with “not covered.”

If you’re a contractor or service business in Willis, Conroe, and Montgomery County, this checklist helps you quickly spot gaps that commonly lead to denied claims or surprise out-of-pocket costs.

Quick note: This is educational only. Every business is different. If you want a fast coverage review, TGH Insurance can walk through your current policies and COI requirements.

The 3-Minute Coverage Gap Scorecard (do this first)

Give yourself 1 point for every “YES.”

At the end, your score tells you what to do next.

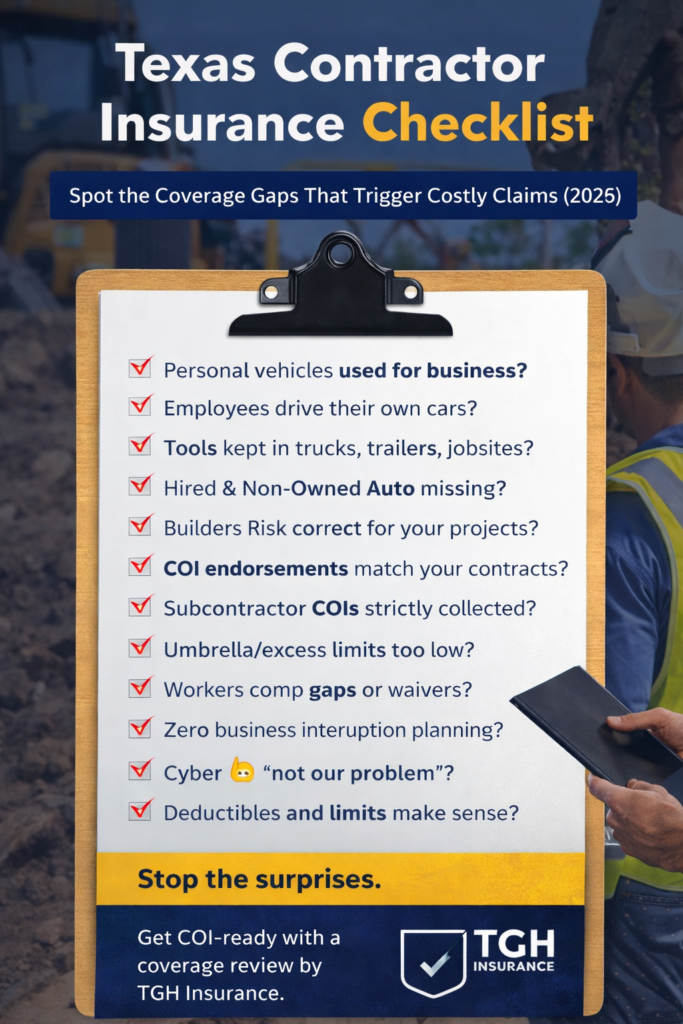

- Do you use any personal vehicles for business errands, sales calls, or hauling tools?

- Do employees ever drive their own vehicles for work?

- Do you keep tools/equipment in a truck, trailer, jobsite, or storage unit?

- Have you added services, locations, or payroll in the last 12 months?

- Have you signed a contract requiring additional insured / waiver of subrogation / primary & non-contributory?

- Would a lawsuit over an injury or property damage be financially painful, even with GL?

- Do you invoice over email, store customer data, or use online payments?

- Could you survive 30–60 days of downtime if a loss shut down operations?

- Do you subcontract any work?

- Would you recognize a coverage gap if your COI got rejected by a GC?

Score guide:

- 0–2: You’re probably okay, but still review annually.

- 3–6: You likely have at least one meaningful gap.

- 7–10: You’re in the danger zone (most claims problems happen here).

12 Coverage Gaps Texas Contractors Get Hit With (and how to fix them)

1) “It’s just one truck” (but it’s used for business)

If a vehicle is used for business—even part-time—personal auto may not respond the way you expect. A common fix is moving to commercial auto or properly structuring business use.

Red flag: You have signage, carry tools/materials, or employees drive it.

2) Fleet vs. non-fleet confusion

A “fleet” isn’t only for big companies. If you’re adding vehicles, drivers, or using different vehicle types (truck + van + trailer), your setup needs to match your actual use.

Fix: Build your auto schedule and driver setup like you plan to grow—not like you plan to stay small.

3) No Hired & Non-Owned Auto (HNOA)

This is the silent killer.

If employees use their own cars for work (or you rent a vehicle), a crash can come back on the business. HNOA is often the missing piece.

Claim trigger: Employee runs to Home Depot for supplies and rear-ends someone.

4) Tools and equipment aren’t covered where they actually live

Many contractors assume GL covers stolen tools. Usually it doesn’t.

If tools live in a truck, trailer, jobsite, or storage unit, you typically need inland marine / contractor’s equipment coverage.

Claim trigger: Trailer theft at a hotel or jobsite.

5) The deductible + limit mismatch nobody notices

Your policy might exist, but the deductible/limit might be out of sync with your reality.

Example: $1,000 deductible for small losses is fine… until you’re dealing with repeated tool theft or minor auto losses.

Fix: Choose deductibles/limits based on frequency and severity.

6) Builders Risk is missing—or written wrong

If you’re building or renovating, builders risk can be essential. But it must match:

- the project type

- who is responsible (you vs. owner vs. GC)

- the contract language

Claim trigger: Storm damage or theft of materials before install.

7) General Liability doesn’t match your contracts

A lot of COIs get rejected because the GL policy doesn’t support what your contracts demand.

Common COI requirements:

- Additional insured wording

- Primary & non-contributory

- Waiver of subrogation

- Specific endorsement forms

Fix: Don’t wait until the COI is rejected—review contract language up front.

8) Subcontractor risk isn’t controlled

If you subcontract work, you need a simple but strict process:

- COI collection (every sub, every renewal)

- Correct limits

- Additional insured where required

- Clear scope language

Claim trigger: Sub causes damage; your policy responds first because their coverage was missing/inadequate.

9) No umbrella/excess (or it’s too small)

GL + Auto limits can get burned up fast. An umbrella is one of the most cost-effective ways to increase protection.

Rule of thumb: If a claim could exceed your base limits, you should at least price an umbrella.

10) Workers comp assumptions

Texas is different than many states. Whether you carry workers comp or not, you need to understand your exposure and what your contracts require.

Fix: Align your setup with: your payroll reality, your jobsite requirements, and your risk tolerance.

11) Business interruption is ignored until it’s too late

If a loss shuts you down, you don’t just lose equipment—you lose time, revenue, and momentum.

Fix: Review business interruption options and what actually triggers it in your situation.

12) Cyber is “not our problem” (until invoice fraud hits)

Contractors get hit by:

- invoice/bank-change scams

- email compromise

- ransomware

- customer data exposure

You don’t have to be a tech company to have a tech-based loss.

Fix: At minimum, review cyber options + basic email/payment controls.

A simple “what you should do next” plan

If you scored 0–2

Do an annual review and keep your COIs organized.

If you scored 3–6

Pick the top two gaps that could create the biggest financial hit (usually Auto + Tools/Equipment or HNOA).

If you scored 7–10

Book a full review. The goal isn’t more coverage—it’s the right coverage that matches contracts and operations.

Want us to run this checklist against your real policies?

At TGH Insurance, we help contractors and service companies in Willis, Conroe, and Montgomery County spot gaps before a claim happens.

Request a proposal or coverage review and we’ll walk through:

- current policies + limits

- COI requirements from your biggest clients

- vehicle use + driver setup

- tools/equipment exposure

- the fastest fixes that reduce risk without overpaying

FAQ (SEO-friendly)

Do I need commercial auto insurance in Texas if I only have one truck?

If it’s used for business (tools, hauling, employees driving, jobsite use), commercial auto is often the safer structure than a personal policy.

What is Hired & Non-Owned Auto (HNOA)?

HNOA helps cover liability when employees drive their personal vehicles for business or when you rent/borrow vehicles for work.

Does general liability cover stolen tools?

Often, no. Tools/equipment theft usually falls under inland marine/contractor’s equipment, depending on where items are stored/used.

What’s the easiest way to avoid COI rejections?

Review contract requirements early and make sure your policy endorsements support what the GC requests.

Willis, TX 77318